The truth is uncomfortable, yet deeply real. The middle class is the most disciplined, responsible, and dependable segment of India. They wake up early, commute through traffic, manage family responsibilities, pay their EMIs on time, and rarely complain. They follow the rules. They believe in education. They believe in stability. They believe that if they keep working hard, life will eventually reward them.

But here is the question that most people avoid asking: what happens when the rules of the game change?

For decades, discipline and hard work were enough. A stable job meant stability in life. Savings in the bank meant security. A degree meant respect and upward mobility. But the world has shifted. The system has evolved. Markets have transformed. Technology has redefined value. And yet, most middle-class families are still playing by yesterday’s rules.

That is where the trap begins.

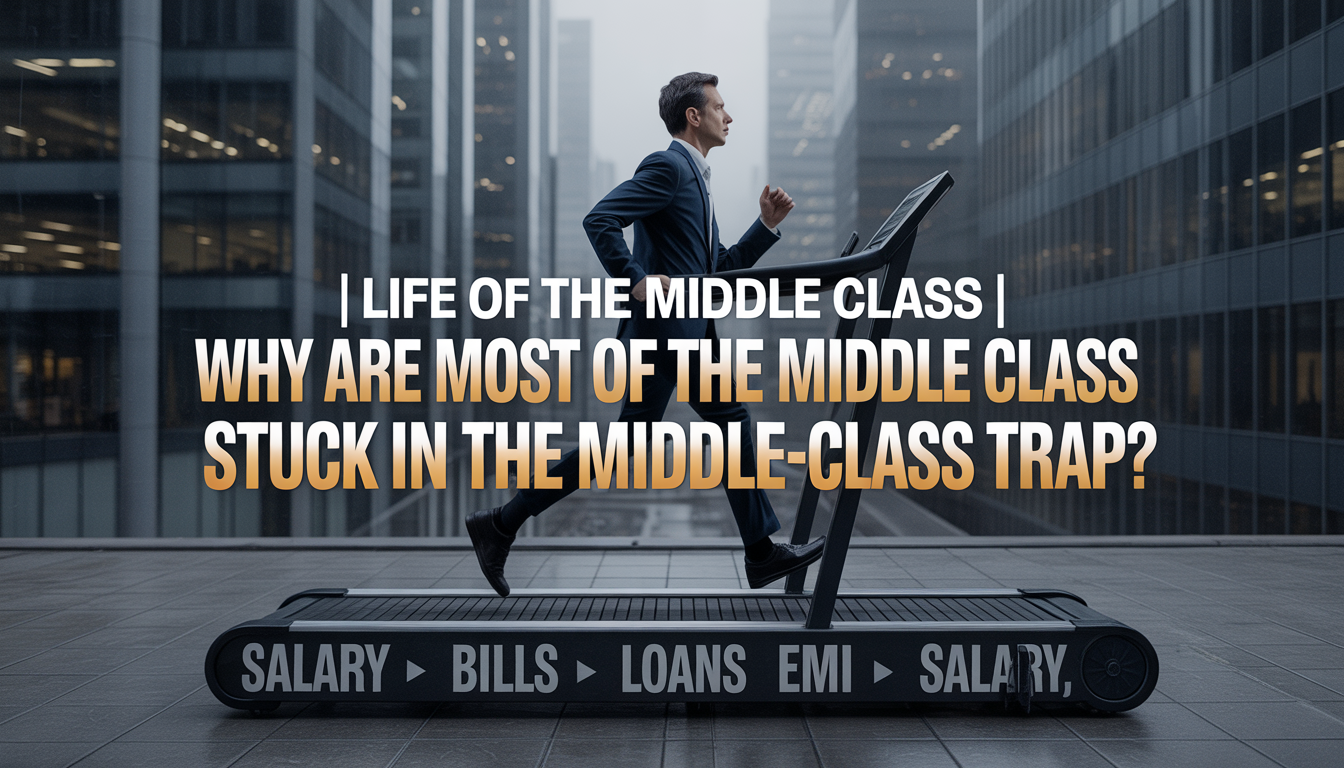

The Discipline That Became a Cage:

The middle class has always believed in structure. Study hard. Get a good job. Avoid unnecessary risks. Save money. Buy a house. Secure your children’s future. This formula worked in a predictable economy. But today’s economy is not predictable. It is volatile, global, and deeply interconnected.

Discipline is powerful. Responsibility is admirable. But when discipline turns into rigidity, it becomes a cage. When hard work is not combined with adaptability, it slowly loses its edge. Many middle-class professionals continue repeating the same moves, same job patterns, same saving strategies, same financial habits, even though the environment around them has dramatically changed.

The problem is not laziness. The problem is repetition without reflection.

You can work sincerely for 25 years. You can avoid all obvious mistakes. You can stay loyal to your employer. And yet, you might still feel stuck. Promotions slow down. Salaries barely beat inflation. Expenses rise faster than income. The discipline remains. The growth does not.

The Silent Risks Nobody Talks About:

When people think about risk, they usually imagine stock market crashes or business failures. But today’s biggest risks are silent. They do not make headlines. They do not create drama. They slowly eat away at stability.

Inflation is one such silent force. Prices rise gradually, almost invisibly. What you could buy comfortably five years ago now feels expensive. School fees increase. Medical bills increase. Rent increases. Lifestyle expectations increase. Income may increase too but not always at the same pace.

Currency depreciation adds another invisible pressure. In a globalized world, where products, services, and even aspirations are international, the value of money matters more than ever. When the currency weakens, global goods become more expensive. Travel becomes expensive. Imported technology becomes expensive. Even education abroad becomes distant.

Then there is single-income dependency. Many middle-class families rely heavily on one primary earner. That creates vulnerability. A job loss, a health crisis, or a business slowdown can destabilize the entire household. Stability that looked solid suddenly becomes fragile.

And perhaps the biggest issue: zero or minimal asset ownership. Many people spend decades earning, but do not build appreciating assets. Salary is active income. It stops when you stop working. Without ownership of businesses, equity, intellectual property, or scalable assets, financial growth remains limited to increments and bonuses.

These risks are already active. You do not need to take any action for them to affect you. They are working silently in the background.

The Illusion of Safety:

One of the most powerful beliefs in the middle class is the belief in safety. A government job is safe. A corporate job is safe. Fixed deposits are safe. Avoiding risk is safe.

But is it truly safe?

The world is increasingly automated. Artificial intelligence is reshaping industries. Global companies can hire talent remotely from anywhere. Corporate loyalty has decreased. Job security is not what it used to be. Even traditional sectors are experiencing disruption.

The question, therefore, should not be whether investing is safe or risky. The real question is: what risk are you willing to take?

Because doing nothing is also a risk. Staying dependent on one income stream is a risk. Ignoring wealth creation is a risk. Avoiding financial education is a risk. Pretending that the future will look like the past is perhaps the biggest risk of all.

Middle-class families often avoid visible risk while unknowingly accepting invisible risk. They fear market volatility but ignore inflation. They fear entrepreneurship but ignore career stagnation. They fear failure but ignore slow decline.

Safety, in many cases, is just comfort in disguise.

Participation Without Ownership:

Every day, millions of middle-class Indians contribute to the global economy. They use global platforms. They scroll through WhatsApp. They spend hours on Instagram. They watch videos on YouTube. They generate data. They create engagement. They consume content. They support advertising ecosystems.

But what do they own in return?

Most people are participants, not stakeholders. They are users, not shareholders. They are employees, not equity holders. They are consumers, not creators.

The global economy rewards ownership disproportionately. Founders, early investors, shareholders, and intellectual property holders benefit from scale. Users and employees benefit, but often in limited ways.

Think about it carefully. You may be deeply integrated into the global digital ecosystem. Your time, attention, and data are valuable. But unless you have ownership shares, businesses, skills that scale globally, or digital assets, your participation may not translate into wealth creation.

This is not about blaming anyone. It is about awareness.

The Middle Class Identity Trap:

There is also a psychological dimension to this trap. The middle class often defines itself through stability and respectability. Risk-taking can feel irresponsible. Entrepreneurship can feel uncertain. Investing can feel intimidating. Changing careers can feel dangerous.

Over time, identity becomes a boundary. “People like us don’t do that.” “Business is not for our family.” “Markets are for the rich.” “We are simple salaried people.”

These narratives protect comfort, but they also limit growth.

The irony is that the middle class has the highest potential for transformation. They are educated. They are disciplined. They understand delayed gratification. They value learning. If these traits are redirected toward financial literacy, asset creation, and strategic risk-taking, the impact can be massive.

But first, the mental shift must happen.

Hard Work Is Not Enough Anymore:

Hard work remains important. Discipline remains important. Responsibility remains important. But they are no longer sufficient on their own.

Today’s world rewards leverage. Leverage of capital. Leverage of technology. Leverage of networks. Leverage of knowledge. Someone working ten hours a day in isolation may earn less than someone who builds a system that works even when they sleep.

This does not mean everyone must become an entrepreneur. It means everyone must understand how value is created in the modern economy. How companies scale. How equity works. How compounding works. How digital assets work. How skills can be monetized globally.

Without this understanding, even sincere effort may not produce desired outcomes.

Trap of Stagnation:

The trap is not poverty. The trap is stagnation.

A Pause, not a conclusion. This is not a dramatic warning. This is not a conclusion. It is a pause.

The middle class is not weak. It is not lazy. It is not incapable. It is simply operating with outdated assumptions in a rapidly evolving system. The real question is personal.

What part are you actually becoming in the global economy?

Are you only a consumer? Only an employee?

Only a silent contributor? Or are you gradually becoming an owner, an investor, a creator, a stakeholder?

You are already participating. That is unavoidable. The real choice lies in how you participate. Think for yourself. Reflect on your income sources. Reflect on your assets. Reflect on your risks, both visible and invisible. Reflect on whether your current strategy is based on today’s realities or yesterday’s comfort. The middle-class trap is not a conspiracy. It is a pattern. And patterns can be changed, but only when they are recognized.

This is your pause. Now, the question is yours.

Conclusion:

The middle-class trap is not created by a lack of effort; it is created by a mismatch between effort and direction. For decades, discipline, stability, and hard work were enough to ensure progress. But today’s world operates differently. It rewards adaptability, ownership, and leverage more than routine and predictability.

The uncomfortable truth is that many middle-class individuals are not failing; they are simply playing a game whose rules have already changed. Continuing to rely only on a fixed salary, traditional savings, and risk avoidance may provide short-term comfort, but it often leads to long-term stagnation. Meanwhile, silent forces like inflation, technological disruption, and global competition continue to reshape financial realities.

Breaking out of this trap does not require abandoning discipline; it requires upgrading it. The same consistency that once built stable careers can now be used to build assets, learn new skills, invest wisely, and create multiple income streams. The goal is not reckless risk-taking, but informed and strategic participation in the modern economy.

Ultimately, the shift is both practical and psychological. It is about moving from security to growth, from consumption to ownership, and from routine to awareness. The middle class has the potential, the mindset, and the resources to evolve, but only if it questions its long-held assumptions.

This is not about fear. It is about clarity. You are already part of the system. The real question is whether you will remain a passive participant or become an active creator of your financial future.

FAQs

1. What exactly is the “middle-class trap”?

The middle-class trap refers to a situation where individuals earn enough to live comfortably but struggle to build long-term wealth. They rely heavily on salaries, have limited assets, and are affected by rising costs, preventing financial growth despite consistent effort.

2. Is hard work no longer important?

Hard work is still important, but it is no longer sufficient on its own. In today’s economy, combining hard work with smart strategies like investing, skill development, and leveraging technology is essential for real financial progress.

3. Why is relying on a single income risky?

A single income creates dependency. If that income stops due to job loss, health issues, or economic changes, financial stability is immediately threatened. Multiple income streams provide security and flexibility.

4. How can someone start moving out of the middle-class trap?

Start by improving financial literacy, investing in assets (like stocks, businesses, or skills), diversifying income sources, and staying adaptable to market changes. Small, consistent steps toward ownership and growth can create long-term impact.

5. Is investing and taking risks necessary for growth?

Yes, but the key is calculated risk, not reckless decisions. Avoiding all risk can be more dangerous in the long run due to inflation and stagnation. Learning to manage and take informed risks is essential for financial advancement.